This is the third and final part in our series on achieving hyper-personalization of content at

scale.

In our previous articles, we addressed the macro trends shaping the wealth management

industry and how the hyper-personalization of content is instrumental to craft the unique

experiences customers are demanding (part 1). We then began to answer the question “How

does a smart content management solution look like?”, and deep-dived into the common

challenges associated with content creation and matching to customer profiles (part 2). Today,

we will continue to address this question by looking at the two other pillars of a smart content

management solution: distribution and the feedback loop.

DISTRIBUTION – DELIVERING CONTENT THROUGH THE RIGHT CHANNEL, IN THE

RIGHT FORMAT

Content creation is the foundation for a good content management strategy on which matching

capabilities can be built and incrementally ameliorated. This is only half the journey, as content

needs to reach the clients and prospects. Personalization means not only delivering the right

content, to the right people, at the right time but also through the right channel and in the right

format. It is about offfering tailor-made experiences that keep users engaged by showcasing

content on their preferred channels. Hence. omnichannel distribution¹ is an integral part of the

hyper-personalization of the customer experience, which enables wealth management firms to

reinforce their brand’s stickiness and increase overall engagement with their marketing and

research efforts.

Smart content management solutions do not add new channels but make channel-ready content

available to be effortlessly distributed through the existing ones. As the adaptation of the content

to the channels is automated and no longer borne by content creators or RMs, the addition of

new channels – e.g., locally preferred channels like WeChat to serve Chinese clients – is fostered.

Yet, distribution often suffers from the limitations of the two pillars aforementioned. The most

common shortfall that we observe amongst financial institutions is that they do not leverage

enough on their existing channel. This is precisely because they lack the processes and tools to

identify clients’ preferred channels, and adapting content that has not been created formatneutral is time consuming and error-prone.

Consequently, wealth management firms mainly rely on ‘PDF journeys’, where content pieces are

manually created and saved in a static PDF format, that would restrict the customer experience

on channels like mobile or e-banking apps or chat, and lacks the analytics that is so important to

sustain the smart content model as we will elaborate in our next paragraph. This is well reflected

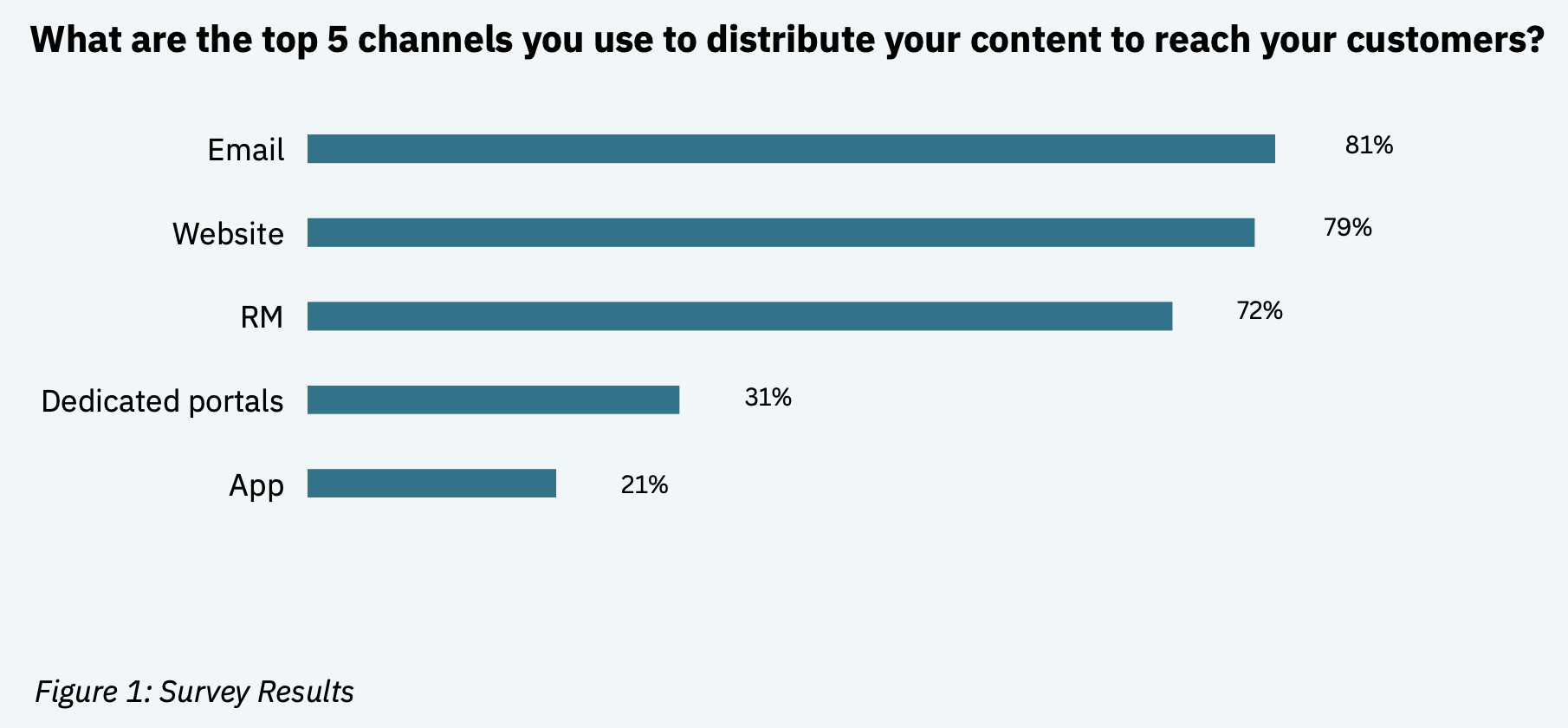

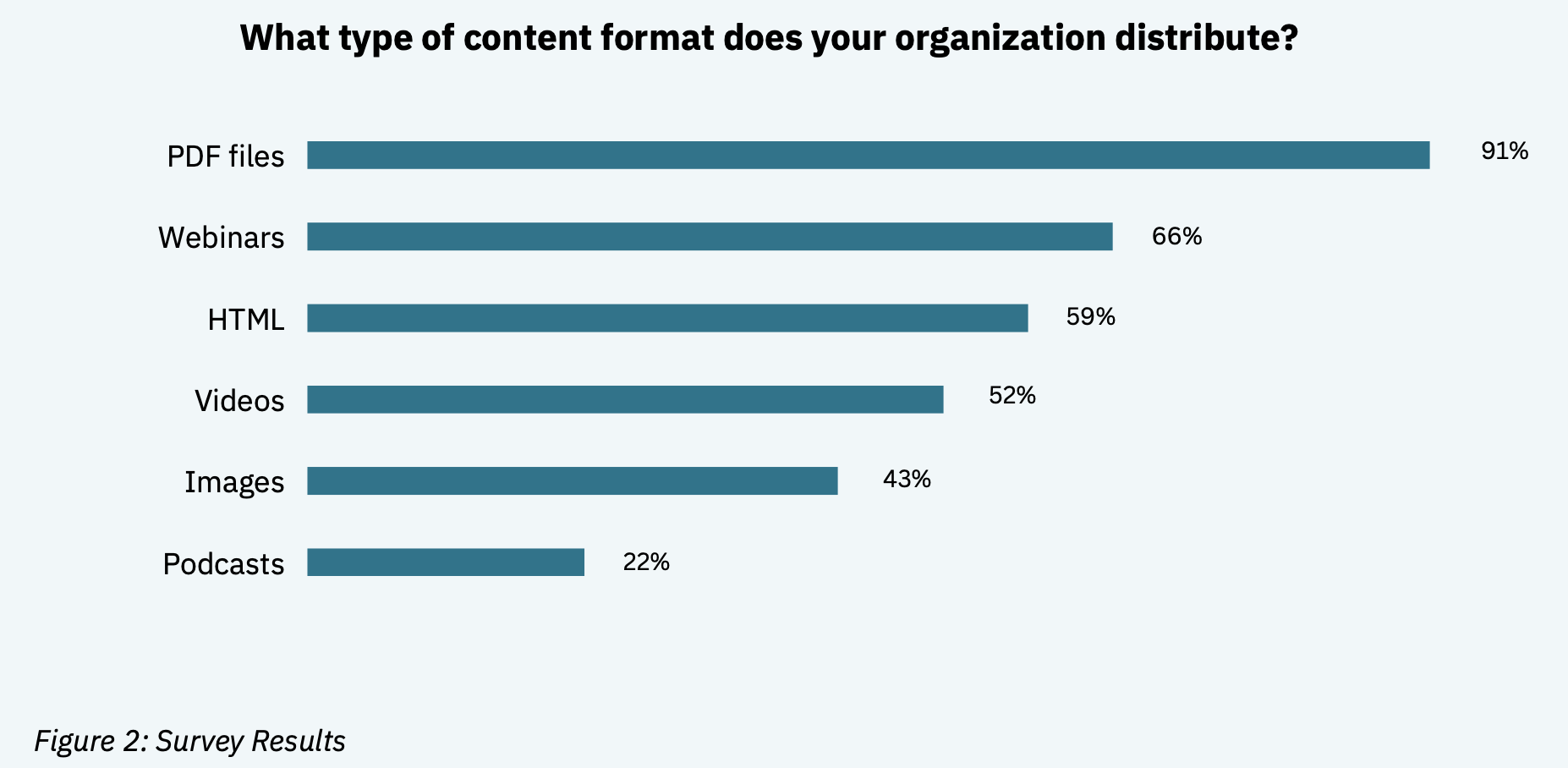

in our survey with email being the most-used channel amongst our surveyors (see figure 1

below), and PDF being the most-used format (see figure 2 below). In such instances, the content

is either mass distributed with little to no personalization (retail, mass affluent or underserved

HNWI), or manually matched and personalized by the RMs (HNWI and UHNWI).

Solution

So, how should financial institutions tackle distribution as part of their smart content

management solutions?

As a first step, we believe that a distribution strategy needs to be (re)defined, which should

answer the following questions: Which channel do we want to distribute content through? Which

content is promoted via which channel? How is the content adapted to the channels and to

clients’ preferences? What is the role of the RMs? Traditionally, building such a strategy involves

the creation of user journeys – not only for prospects and clients but also RMs, who are

consumers of certain internal channels (such as content hubs) – and user personas.

To fully leverage the smart content management solution, this must be done in a holistic

approach that considers all products and services (beyond the sales arena), and all channels:

print vs. digital, manual vs. automated vs. subscription-based distribution, and push vs. pull. As

stated in our previous articles, we advocate for a hybrid human-machine model that empowers

the RMs to better serve clients. In practice, this means that content can be distributed

automatically to clients and/or manually pulled by RMs to be distributed to selected clients. RMs

can access a research portal to browse available content (via a simple content hub web portal)

and individualise publications. Ideally, they should be able to view which content has been

distributed to which client and see undistributed matched content that could be of interest for

the client and why – e.g., “similar profiles like this”, or “based on client subscription”.

This channel strategy must feed the content creation pillar, as the rendering requirements should

be adjusted to each specific channel; as well as to the matching engine for the selection of the

relevant channel for each client (rule-based model as per the defined personas). The smart

content management solution will orchestrate the distribution of content via the appropriate

available channels. Here again, actors can start the implementation by plugging in only selected

channels to their smart content management solution, and gradually add more channels to the

mix.

Just as the matching capability starts as manual process, before evolving to a static rule-based

model and eventually an AI-powered engine; personas are used as a baseline for defining the

distribution strategy. Personas are essentially educated guesses on a general audience and a

representation of what a customer within a target segment looks like. To elevate the offering

towards true hyper-personalization, Content Managers need to map out a more accurate

customer journey based on granular, person-level insights from actual customers, derived from

omnichannel measurements and analytics: the feedback loop.

The feedback loop can be defined as a unified engagement measurement strategy that allows

banks to understand the reach of its content in the different channels and the popularity of the

created content. The matching capability and the feedback loop are two sides of the same coin.

Client data must be leveraged to glean – meaningful insights into customer preferences and

behaviors; and fueled back to the matching engine. Easier said than done. Banks and financial

institution have access to huge amounts of customer data, that are often untapped due to legacy

technology and data silos across the bank. The unification of data is critical and should not be

overlooked when implementing smart content management solutions. Incomplete data can

severely limit and even undermine your personalization strategy. Figure 3 on the next page shows

that our respondents have mentioned “Disparate technology systems and data” as the biggest

challenge they face for a more integrated approach to content management.

THE FEEDBACK LOOP – THE CORNER STONE FOR A SMART CONTENT MANAGEMENT

Solution

To take the edge off this challenge, banks must build a comprehensive data infrastructure with two components:

- Inputs, i.e., means to capture data (data points) across all customer touchpoints, that can potentially be enriched with third-party data;

- A platform that unifies all analytics data in one place that allows for a 360-degree view of customer profiles.

Ideally, analytics should connect the dots between client engagement through content, and its impact on overarching metrics such as trades volume, share of customer wealth invested to the bank or customer satisfaction (Net Promoter Score). A good practice is to share those metrics transparently to all the stakeholders involved in the content management value chain, and to share accountability on the results. For example, feedback like most popular topics can be used by content creators as input to refine topics to address, or drop off point to update how content is shown on certain channels. This makes sure all teams are aligned towards the same goals and avoid silo-thinking – Stakeholders can view when individual channels are at their most effective, what messages are resonating, and how each channel contribute to the bank’s success.

A few steps that can be taken towards the implementation of the feedback loop are:

- Determination of activity tracking requirements

- Definition of metrics and KPIs to measure efficiency

- Creation of a data model

- Aggregation & Reporting

CONCLUSION

To conclude, the feedback loop is instrumental to fuel the AI-powered matching engine and practice recursive learning, which is the capability to constantly learn about each of your clients and adjust based on real-time events and actions. This is what eventually allows financial institutions to move from “persona to person” and sustain the delivery of hyper-personalized experience via smart content management solutions.

We strongly believe that customer data will be the next battleground for wealth management firms that aims at building a competitive advantage by crafting and delivering unique experience to their clients.

If you would like to discuss how to implement a smart content management solution that unlocks the value of your clients’ data and leverage it to create a hyper-personalized customer experience, then let’s start a conversation.

About finalix

Finalix is a consulting boutique with a focus on the financial industry. Originating from Switzerland, the company was founded in 2001 and opened an office in Singapore in 2019.

Finalix supports a wide range of financial services providers from banking – universal banks, private banks, asset managers, and private equity corporations – to insurance. The company focuses on digitisation and transformation projects covering key senior roles on the business side as product owners, SMEs and stream leads. Finalix consultants have on average more than 12 years of significant work experience with renowned consulting companies and senior roles in the financial services industry. They bring strong skill sets, fast adaptability to new environments, and instant value delivery to their projects.